Investors shifted to rotational play into mid- and small-cap segments, favouring domestically driven and higher-beta names with clearer earnings visibility.

IPPFA Sdn Bhd director of investment strategy and country economist Sedek Jantan said despite initial gains, the benchmark index retreated into negative territory as buying interest in large-cap names faded, suggesting that early positioning was not supported by sustained institutional flows.

“While the telecommunications sector continued to draw attention after Telekom Malaysia announced an upward revision to its dividend payout policy to a minimum of 75% of profit after tax and minority interest on a quarterly basis, the support proved insufficient to anchor the broader index.

“The intraday fade reflects not just profit-taking, but a more structural hesitation to build exposure in large caps amid an uncertain external backdrop,” he added.

Sedek said that the FBM70 and FBM Small Cap indices both closed higher, extending their uptrend and signalling a continued rotation of capital into mid-and small-cap segments.

This divergence highlights a more nuanced market dynamic, where investors are selectively reallocating towards domestically driven and higher-beta names with clearer earnings visibility, rather than exiting the market altogether.

“At the macro level, sentiment remains highly sensitive to geopolitical developments, particularly around the Strait of Hormuz,” he added.

Meanwhile, Rakuten Trade Sdn Bhd vice-president of equity research Thong Pak Leng said the equities broker maintained a cautiously optimistic view, as the benchmark index has managed to stay above the 1,700 level, with signs of buying support emerging after the recent pullback.

“The rebound from around 1,680 suggests that investors are willing to accumulate on dips, although the market is now approaching a resistance zone near 1,730, where gains may slow,” he said.

Thong said that the index is expected to trade within the 1,700-1,740 range for the week.

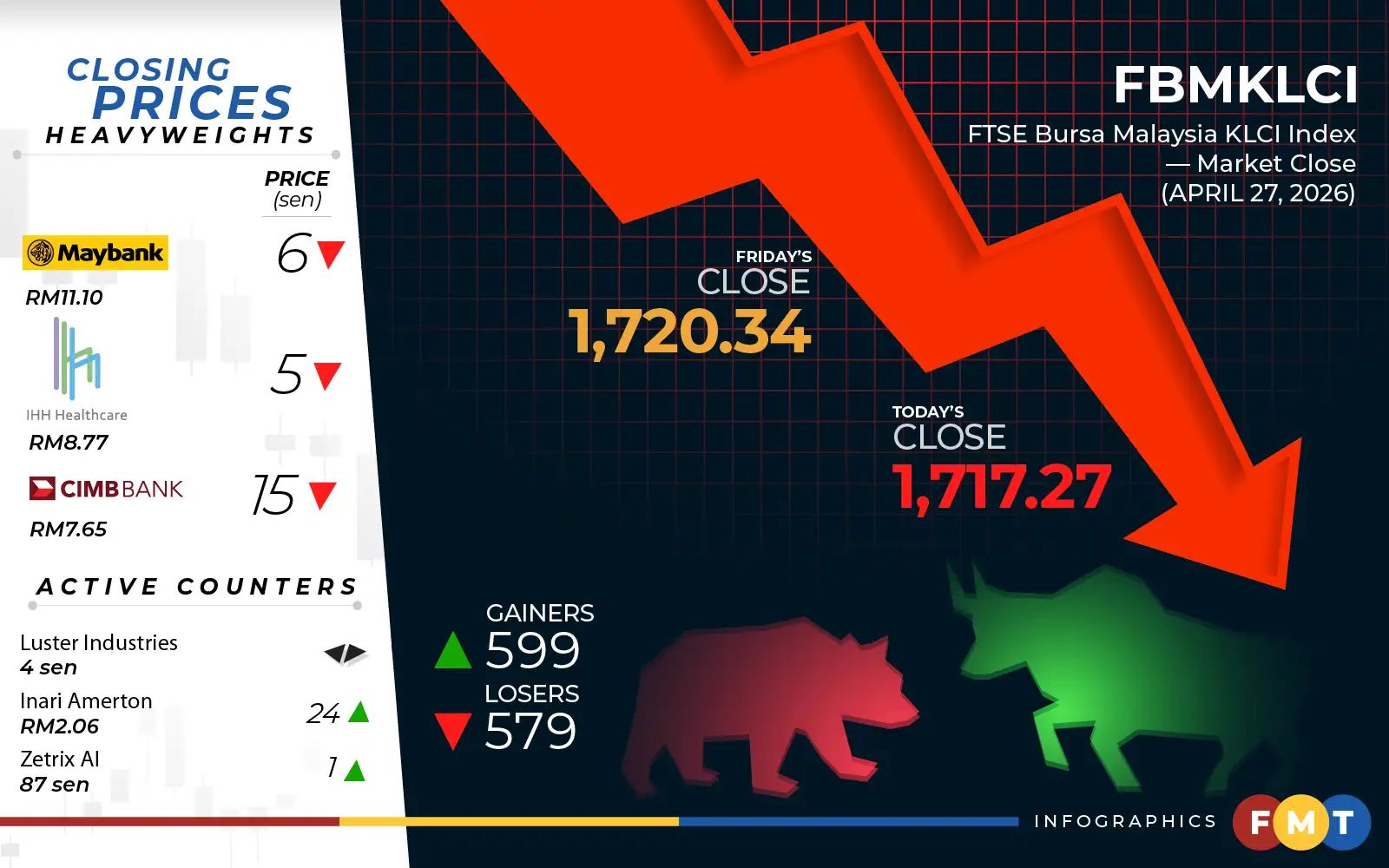

At 5pm, the FTSE Bursa Malaysia KLCI (FBM KLCI) eased 3.07 points, or 0.17%, to close at its intraday low of 1,717.27 from last Friday’s close of 1,720.34.

The benchmark index opened 4.13 points higher at 1,724.47 and moved as high as 1,731.79 in the early morning session.

In the broader market, gainers led losers 599 to 579, while 617 counters were unchanged, 953 untraded and 67 suspended.

Turnover expanded to 3.74 billion units valued at RM3.30 billion from 3.22 billion units valued at RM3.25 billion last Friday.

Among heavyweights, Maybank fell 6 sen to RM11.10, Public Bank was 9 sen lower at RM4.72, Tenaga Nasional was 8 sen easier at RM14.58, CIMB slid 15 sen to RM7.65 and IHH shed 5 sen to RM8.77.

On the most active list, Luster Industries was flat at 4 sen, Inari Amerton gained 24 sen to RM2.06, Zetrix AI perked up 1 sen to 87 sen, VS Industry was flat at 22.5 sen, and AirAsia X lost 1 sen to RM1.24.

Top gainers were led by Telekom Malaysia, which garnered 48 sen to RM7.58, F&N and Press Metal were 38 sen higher at RM30.68 and RM8.80, respectively, Unisem climbed 22 sen to RM3.30.

As for top losers, United Plantations dipped 70 sen to RM31.62, Hong Leong Bank was 44 sen lower at RM22.34 and Hong Leong Financial slipped 30 sen to RM19.0.

On the index board, the FBM Emas Index edged up 0.41 of-a-point to 12,716.13, the FBMT 100 Index ticked up 0.09 of-a-point to 12,549.39, the FBM Emas Shariah Index climbed 73.47 points to 12,660.09, the FBM 70 Index increased 96.64 points to 18,169.07, and the FBM ACE Index added 5.70 points to 4,658.02.

By sector, the financial services index dipped 245.90 points to 19,976.91, the industrial products and services index edged up 2.55 points to 194.91, the energy index perked up 1.30 points to 831.61, while the plantation index declined 10.68 points to 8,834.57.

The Main Market volume rose to 2.32 billion units valued at RM3.01 billion from 1.80 billion units valued at RM2.94 billion last Friday.

Warrants turnover slipped to 1.01 billion units worth RM141.36 million from 1.02 billion units worth RM147.79 million previously.

The ACE Market volume expanded to 409.6 million units valued at RM154.98 million from 396.83 million units valued at RM160.00 million registered on Friday.

Consumer products and services counters accounted for 286.26 million shares traded on the Main Market, industrial products and services (735.6 million), construction (190.24 million), technology (435.62 million), financial services (71.15 million), property (192.2 million), plantation (28.54 million), real estate investment trusts (17.08 million), closed-end fund (28,300), energy (136.72 million), healthcare (73.41 million), telecommunications and media (86.85 million), transportation and logistics (34.52 million), utilities (33.83 million), and business trusts (219,100).

Meanwhile, Bursa and its subsidiaries will be closed on May 1, 2026, in conjunction with the Labour Day public holiday.

The stock exchange and its subsidiaries will resume operations on May 4, 2026.